I'm Cao Jiang, co-founder of Omni-Growth Agent, an AI overseas marketing agent. The first wave of customers we've worked with includes a number of established Amazon sellers building (or trying to build) their own DTC sites. The question they ask me most often is simple: "Is the independent DTC site still worth doing?"

The anxiety isn't manufactured. Late March 2026, Allbirds — once a $4B+ IPO darling — sold to American Exchange for $39M. Of 22 publicly listed DTC brands, more than half have lost over 50% of their value.

It's a hard question to answer.

Intuition is useless. PR releases and founder interviews are also insufficient — they're filtered through self-attribution and survivorship bias. So I had an AI agent scan public sources for ~300 DTC death signals, then narrow down to 167 named cases for closer post-mortem.

The 300+ figure is the raw pool from public reports, including anonymous and fuzzy entries. The validated, named cases that ultimately drove the analysis: from Allbirds and Casper (repeatedly named in legacy media) to Chinese cross-border veterans like RAVPower (parent: Sunvalley) and Anker subsidiaries, down to anonymous Reddit posters who'd burned $5,000 on a Shopify store.

When the data came back, I stared at the pie chart for a few seconds: 95.5% of cases died from the same single mistake — running a DTC site with Amazon's "buy traffic, get orders" PPC reflex.

This article covers two things: (1) how an AI agent and I assembled this analysis in roughly half a day, and (2) what the failure dataset is telling Amazon-to-DTC pivots about their next 12 months.

1. Why a Failure Dataset Beats Studying Winners

I led the engineering side of Sensors Data for eleven years, working with hundreds of customers making data-driven decisions. The gap between "decide on instinct" and "decide on data" compounds across years into orders-of-magnitude difference. So when I started Omni-Growth, I gave myself a rule: every customer-facing recommendation has to start from data.

"Is DTC still worth doing?" is, underneath, a very specific question: how does an Amazon seller building DTC differ from a native DTC brand building DTC?

The difference is large.

Amazon muscle memory is a tight PPC loop — search term, bid, listing optimization — that's worked for a decade. DTC isn't that. DTC needs owned audience, SEO, repeat purchase mechanics, brand equity. The trap: an Amazon seller's first instinct on a slow DTC week is, almost always, "spend more on ads."

Whether the path actually works isn't answered by a few celebrity success stories. The honest answer comes from auditing what's already failed, systematically, across the public record.

The short version: before you walk the path, look at how the people ahead of you fell off it.

2. How the AI Agent Scanned 300 Cases

2.1 Four Data Sources, Cross-Validated

Single-source analysis on DTC failures has known blind spots: legacy media skews to flagship brands, technical archives only confirm "it shut down," traffic data can't infer commercial attribution, and forum threads carry emotional bias.

So the agent pulled four independent sources in parallel. Each source covers the others' weaknesses:

| Source | What it provides | Coverage in this pass |

|---|---|---|

| Trade press & filings | Retail Dive, The Fashion Law, Failory, Modern Retail, Business of Fashion, plus S-1 / 10-K filings for public DTCs | Every case has at least 1 media source |

| Wayback Machine (Internet Archive snapshots) | Last live snapshot date + full historical timeline | 72 cases with complete data (52%) |

| Tech-stack fingerprinting | Snapshot HTML scanned for Shopify, WooCommerce, Squarespace | 25 identified |

| Ahrefs (SEO keyword + traffic analytics) | Organic vs. paid ratio, keyword history, traffic curves | Quota-limited, batched later |

Across four sources, trade press plus Wayback alone is enough to support the headline findings. Ahrefs traffic-structure data is reserved for post-publication validation, not load-bearing for this analysis.

2.2 Three Parallel Research Agents

Running one agent across 300 cases isn't practical: context windows blow out, search queries duplicate, and Chinese-language sources get under-covered. We ran three parallel deep-research agents, each owning a data lane:

- Agent A — Global DTC (English-language press): Retail Dive, Modern Retail, Business of Fashion, Failory, the 5W DTC Graveyard, SEC EDGAR — 75 named cases.

- Agent B — China cross-border (Chinese-language press): Cifnews, 36Kr, Huxiu, NetEase 100EC, Ebrun — 35 cases, including 11 Amazon-to-DTC failures with full disclosures (Patozon, Yikuaipai, Tongtuo, Cross-Border GoodEasy, Jiazhilian, Choies).

- Agent C — Community / anonymous: r/ecommerce, r/FBA, Indie Hackers, Failory founder interviews — 61 cases with founder-disclosed CAC, shutdown timelines, and revenue numbers.

171 raw records total. "Raw" isn't "usable" — two gates next.

13 landmark cases I already knew about (Allbirds, Casper, Outdoor Voices, Hello Bello, Brandless, SmileDirectClub, Lunya, Disco, Glossier, Dollar Shave Club, GlobalEgrow, etc.) were processed separately and aren't in the 171.

2.3 Deduplication and Validation

Gate 1: Dedup. When a case (e.g., Thrasio) appears in multiple agents, keep the row with the richest key_data field.

Gate 2: Validation. Each row must satisfy:

- Verified brand / company name

- Confirmed shutdown date (month-precision for most, year-precision for older or anonymous cases)

- Working URL to a publicly accessible source

- Quantified financials where available (valuation, revenue, burn, CAC, shutdown date, layoffs)

171 raw → minus 6 cross-source duplicates → minus 6 landmark cases (broken out for separate analysis, not pooled) = 159 validated rows, all passing.

Before analysis, the agent and I did a human-review pass on those 159 and removed 5: 4 confirmed alive via a second source (one is Bravo Sierra, expanded in §4.2 below as an active omnichannel pivot success), and 1 anonymous forum thread that doesn't qualify as shutdown evidence. Final dataset: 154 cases in the bankruptcy CSV + 13 landmark cases broken out = 167 named cases total.

2.4 Failure-Mode Attribution

For each of the 167 cases, the agent assigned one primary cause from five candidates: single-traffic-channel, missing repeat purchase, pricing misalignment, product-fit miss, or multi-factor (any combination of the above).

Labeling rubric:

- Media attribution (70% weight): e.g., reports stating "CAC spiked post-iOS 14," "single-product brand with weak repeat."

- Founder post-mortem (20% weight): Failory interviews, LinkedIn essays, Substack write-ups.

- Cross-source data (10% weight): S-1 marketing-spend ratios, Wayback traffic curves.

Cases without strong attribution evidence default to multi-factor.

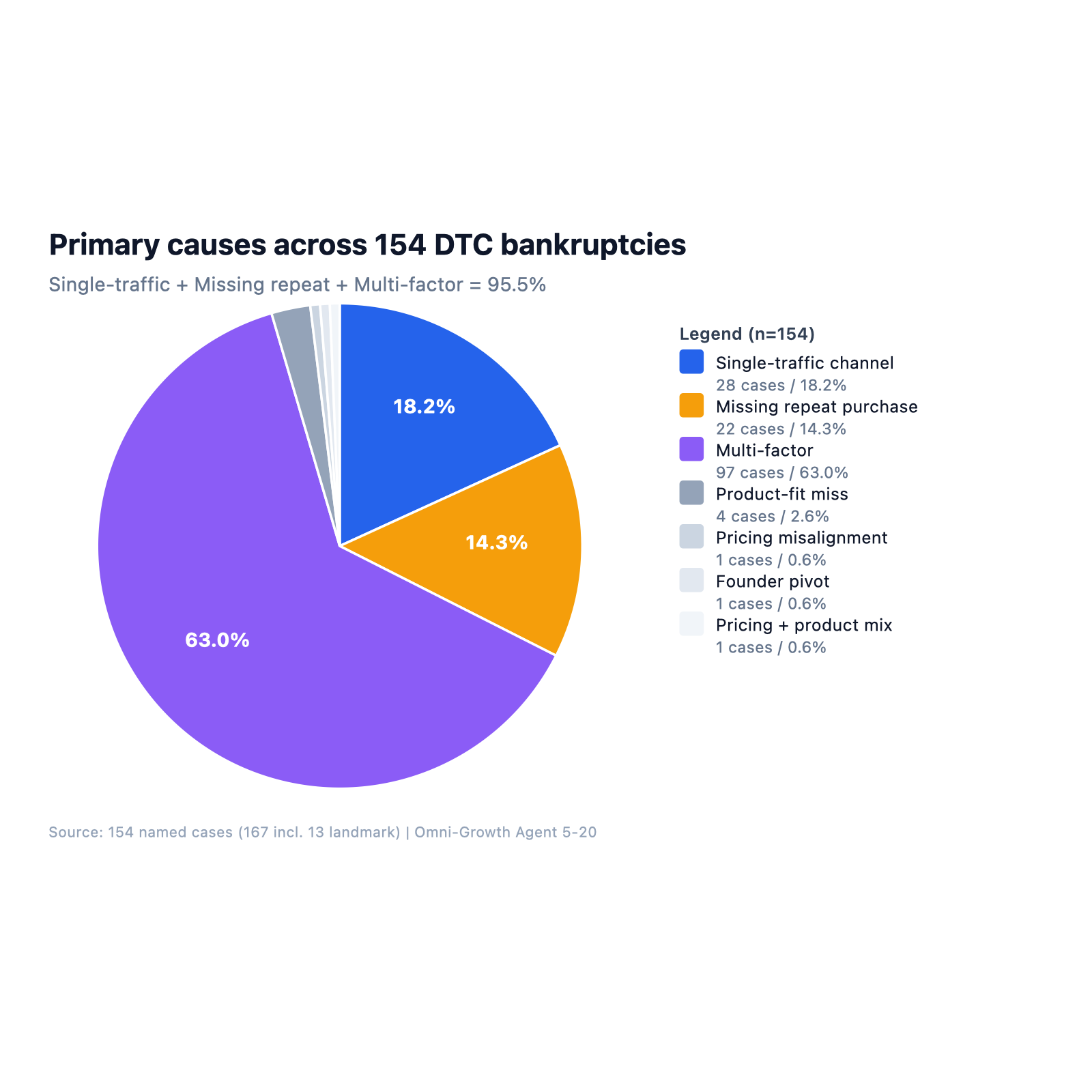

Final result: multi-factor takes 63% of cases, and within multi-factor, the dominant stack is "single-traffic + missing repeat." Single-cause failures are actually rare.

2.5 Every Data Point Is Traceable

Every figure in this article comes from this structured record set.

Each validated row keeps its primary URL, so any data point can be traced back to the original report. After labeling, the agent re-visited each source to confirm numbers hadn't drifted in translation. I've written elsewhere about why this kind of audit trail is non-negotiable when an AI agent makes consequential decisions — the 167-case analysis runs on the same audit principles.

3. The Core Finding: 95.5% on a Single Path

3.1 What Three Charts Show

Percentages below are based on the 154-case bankruptcy dataset.

The chart hits harder than I expected. Single-traffic-channel alone: 18.2%. Missing repeat purchase: 14.3%. Sub-total: 32.5%. I'd expected these two to be the bulk. What I didn't expect: multi-factor at 63% — most cases don't die from one mistake, they die from "single-traffic-channel plus missing repeat" stacked.

Add the three together: 95.5% of DTC bankruptcies trace back to single-channel traffic dependency or missing repeat purchase.

Pricing misalignment is 0.6%. Product-fit miss is 2.5%. Together they're 3.1%.

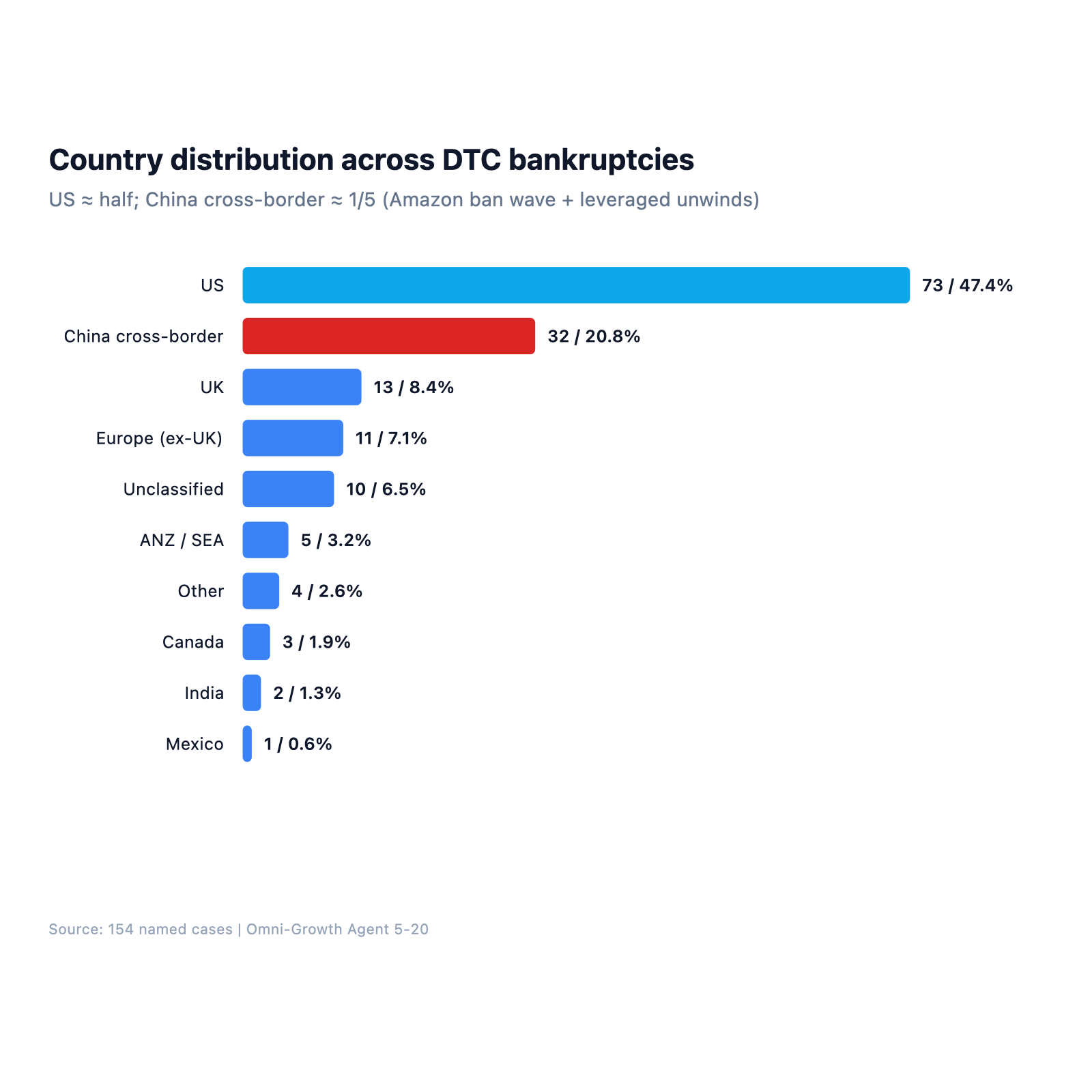

US is nearly half (47.4%). China cross-border is one-fifth (20.8%). The Chinese number carries a hidden story: the 2021 Amazon ban wave shut hundreds of thousands of Chinese seller accounts in a single month, pushing many of them onto DTC sites. Most carried over their Amazon ad-buying reflex — and most didn't make the math work.

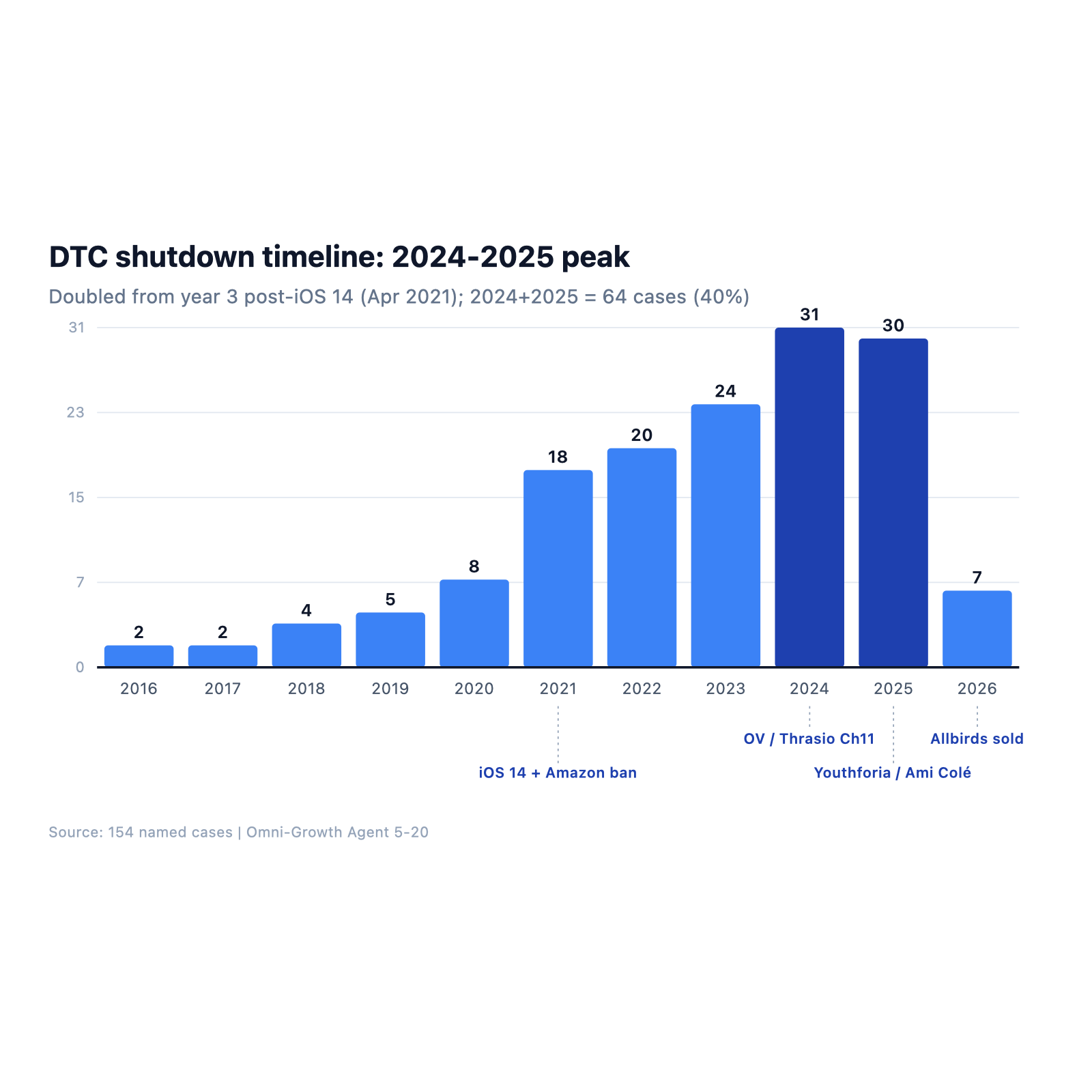

The shutdown curve doubles in 2024-2025. iOS 14 (April 2021) broke Facebook ad attribution; DTC took two to three years to digest the hit.

3.2 Landmark Case 1: Allbirds (Single-Traffic-Channel)

Allbirds is the textbook case for single-traffic-channel.

November 2021 IPO at $4.1B+ valuation. "Eco-friendly wool runners" branding, VC love, Silicon Valley early-adopter crowd. Looked airtight. March 2026 it sold to American Exchange for ~$39M. From $4.1B to $39M — 99% wiped in 5 years.

Where exactly did it break? S-1 numbers are direct: marketing as a share of revenue ran 35–43%. For every $3 of revenue, $1 was buying traffic. The unit economics had no slack — any rise in ad cost or drop in ROI would crack the model.

Then iOS 14 hit (April 2021, seven months before IPO). Facebook ad attribution collapsed, ROI floored. Allbirds had no editorial earned-media cushion (mainstream press rarely featured them organically), no organic search demand (footwear SEO is a brutal long-tail war they didn't win), no repeat purchase (people buy one or two pairs of shoes a year max), and a failed category expansion (apparel got rejected by the market). The moment ad spend stopped, new-customer flow stopped.

Allbirds is single-traffic-channel in its purest form: when you strip away paid acquisition, nothing else carries weight — no earned media, no SEO, no repeat purchase, no brand narrative that pulls new customers in for free. When Apple took the targeting data back, the growth model started cracking; it just took 5 years for the cracks to surface fully.

Modern Retail, Retail Dive, and Bloomberg all converge on this same attribution in their post-mortems.

3.3 Landmark Case 2: RAVPower (Amazon-to-DTC Pivot)

This case hits Amazon sellers hardest because it mirrors the exact path most Amazon-to-DTC pivots try to walk.

Late 2018, RAVPower's parent — Sunvalley — was acquired by Xinghui Precision for ¥1.53B (~$220M), among the first wave of Chinese cross-border IPO bets. Six brands, all running on Amazon FBA.

May 2021: Amazon's global account-ban wave. Sunvalley's six brands lost 330 stores combined — 70.21% of total store count. 2021 revenue dropped 46% YoY, with ¥886M (~$130M) in losses. 2022: another 52% revenue decline, ¥260M in additional losses. Parent company Xinghui's projected 2021 loss: ¥1.24-1.42B. Then in 2024-2025, Italian and French tax authorities issued back-VAT notices (2015-2019 lookback period): €6.4M from Italy, €4.95M from France. Most of the IPO-era asset value evaporated.

Right after the 2021 ban wave, Sunvalley pivoted hard to DTC, trying to rebuild revenue through independent sites. In 2021, non-Amazon channels (own DTC, Walmart, offline) reached ¥605M revenue, up 92% YoY, DTC sales up 30%. Looks like a strong pivot — except it represented just 23.46% of total cross-border revenue. Against the ¥2.58B Amazon base they'd lost, it was a drop in the bucket. Losses deepened year over year.

Why did the pivot fail? Because the playbook that worked on Amazon (stack listings, drive paid review velocity, optimize listing copy) doesn't translate to DTC. On a DTC site, if traffic depends almost entirely on paid ads, with no SEO, no owned audience, no email program; if the product is power banks and earbuds (3-5 year repeat cycle); if brand equity is thin because Amazon listings barely build any — you can't make the unit economics work.

An Amazon seller who knows how to scale Amazon almost always defaults to "buy more ads" when DTC traffic dips. That's the PPC-muscle-memory trap.

Huxiu's post-mortem points to the same root cause: Sunvalley's success depended on early Amazon listing-and-review tactics, and the failure traced back to over-dependence on a single-platform exploit.

3.4 Landmark Case 3: Outdoor Voices (Missing Repeat Purchase)

Outdoor Voices is the textbook case for missing repeat purchase.

Compare the numbers: Outdoor Voices LTV $220, annual order frequency 1.2. Same-category competitor Lululemon: LTV $980, order frequency 4.8. 4.5x LTV gap, 4x repeat-frequency gap.

What does that mean operationally? Outdoor Voices' CAC ceiling is roughly $80 — go above and you're losing money. Post-iOS 14, activewear Facebook CAC ran $80-150 industry-wide. Every new customer was eating 40-70% of LTV.

It's a math problem. High CAC alone is survivable if repeat purchase carries LTV. But Outdoor Voices' "less but better" brand philosophy (premium, no discounts, style over performance) actively suppressed repeat. 1.2 orders a year means most customers bought one pair of leggings and never came back.

Same-category Lululemon survives by stacking community, physical stores, high-frequency activities, and 4.8x annual repeat. Outdoor Voices wanted pure online DTC plus "less is more" purity — the math didn't work. March 2024: all 16 stores closed.

No repeat purchase, insufficient LTV, perpetual traffic-buying. When CAC climbs, the model breaks fast. That's the missing-repeat cascade.

4. Where the Conventional DTC Post-Mortem Goes Wrong

Mainstream DTC commentary tends to converge on a few attributions for the recent failures:

- "DTC is dead, blame the macro and VC pullback."

- "Bad product picks, broken cap tables, saturated market."

- "E-commerce is platform-only now; independent sites have no future."

The data tells a different story.

Across 154 bankruptcy cases, pricing misalignment is 0.6% and product-fit miss is 2.5% — 3.1% combined. Single-traffic-channel, missing repeat purchase, and multi-factor stack to 95.5%.

The translation: most failed DTC sites didn't lose to product or pricing — they lost to operating model. Running a DTC site with Amazon's PPC reflex means buying short-term GMV without building any compounding asset: no owned audience, no email program, no brand narrative, no community. The model held pre-iOS 14 because Facebook ROI was high. Post-iOS 14, attribution broke, Apple took the targeting data back, CAC spiked, LTV couldn't keep up, the equation imploded.

The most counterintuitive datapoint: of the 14 Amazon-to-DTC failures in the dataset, 100% hit either single-traffic-channel or multi-factor. Within this sample, Amazon-trained sellers walking the DTC pivot are most exposed to this specific failure mode — they carry the strongest PPC reflex.

4.1 A Widely-Misread Case: Eloquii

Conventional read: Eloquii was sold off because DTC repeat economics didn't work.

The AI agent pulled a second independent source (TalkBusiness, April 2023, local Bentonville coverage with Walmart-HQ context) and the read flips:

2016: Walmart acquires Jet.com for $3.3B. Jet's founder Marc Lore takes over Walmart's e-commerce, drives a DTC roll-up: Bonobos for $310M in 2017, Eloquii for ~$100M in 2018, plus ModCloth, Moosejaw, and others. 2021: Lore departs. Walmart begins systematically unwinding the entire Lore-era DTC portfolio: 2023 Bonobos sold for $75M (76% haircut), Eloquii sold to FullBeauty, Moosejaw sold to Dick's. These divestitures are different executions of the same strategic decision.

Eloquii didn't fail into its sale. Walmart's strategic retreat from DTC carried it away.

The difference matters. The first read attributes failure to the brand itself, suggesting DTC doesn't work. The second read attributes failure to corporate strategy reversal — DTC may be fine; a 5-year strategic flip from a strategic acquirer wiped it.

For Amazon-to-DTC pivots, this distinction is critical. Many sellers quietly treat "get acquired by a strategic" as plan B: "if we can't scale, at least someone buys us out." Eloquii says: even if you do everything right, even if Walmart pays $100M, a strategic flip 5 years later can package and sell you for parts. Your destiny lives inside the acquirer's strategy cycle, not in your own product strength.

The real lesson: don't underwrite a future on "get acquired by a strategic." Build a DTC that can stand alone, with no external backstop.

4.2 An Overlooked Counter-Example: Bravo Sierra

The other consensus is "DTC is dead, retreat to marketplaces."

The dataset has a clean counter-example: Bravo Sierra killed its Facebook ad spend after iOS 14, pivoted to omnichannel, raised a $17M Series B, and landed in Target and Walmart.

DTC isn't dead. Single-channel paid traffic is dead.

Brands that build the math — LTV, repeat purchase, owned audience — keep working. The failure mode is treating the independent site purely as an ad-buying destination.

5. What This Analysis Can't See

Some limitations worth naming.

What this analysis covers:

- Wayback Machine shutdown dates (52% coverage with full timeline)

- Ahrefs organic vs. paid ratio (quota-bound, batch backfill pending)

- Shopify / WooCommerce platform fingerprinting

- Public media attribution plus S-1 / 10-K filings

What this analysis can't reach:

- Owned audience and email list size: Internal data; not visible to Wayback.

- True COGS and freight contract pricing: Internal supply chain; cross-border logistics is contract-priced.

- Brand narrative and community culture: The unquantifiable layer that AI can't measure.

- Founder factors: Health, family, values, team trust — all qualitative.

One thing worth acknowledging: small brands and anonymous cases are structurally single-source in the public record. When the agent can't find a second corroborating source, that's not AI failure — that's third-party media just not covering this slice of the market. We treat these as "anonymous cases" and don't load-bear primary claims on them.

So this article is about shared failure patterns in a sample, not a single-store diagnostic. For per-store analysis, our agent runs that as a separate workflow — see CTA at the end.

6. Three Lessons for Amazon-to-DTC Pivots

The chain is short: thin traffic mix → missing repeat purchase → CAC climbs → unit economics crack. Running an independent DTC site with the Amazon PPC reflex is the single most common way Amazon sellers lose money on the pivot.

If you're walking that pivot, three concrete lessons from the 167-case dataset:

- Year one: don't bet on "ads in, orders out." Build LTV first. Make the math work before scaling spend.

- Owned audience, email, and repeat mechanics start day one. Not "after we have product-market fit" — they're upstream of the unit economics equation. Without them, paid traffic is a leaky bucket.

- SEO and content are long-term compounding assets, not optional decoration. The brands that survived iOS 14 were the ones with non-paid traffic already running. Building this takes 12-18 months; starting later means missing the window.

These three are unsexy. The 167-case answer is just this plain.

Frequently Asked Questions

Why analyze 300 DTC failures instead of studying successful brands?

Success stories are filtered through self-attribution and survivorship bias. PR releases and founder interviews shape narratives in flattering ways. Failure cases — especially those with public press coverage, Wayback Machine timelines, and S-1 / 10-K filings — get closer to the truth. The headline finding (95.5% of 167 named DTC failures share the same root cause) is invisible if you only study winners.

How was the 95.5% figure calculated? What attributions are included?

95.5% = single-traffic-channel (18.2%) + missing repeat purchase (14.3%) + multi-factor (63%). Most multi-factor cases are "single-traffic + missing repeat" stacked. The agent labeled each case using media attribution (70% weight) + founder post-mortems (20%) + cross-source data (10%, e.g. S-1 marketing spend ratios, Wayback traffic curves). Cases without strong evidence default to multi-factor. The remaining 3.1% breaks down to pricing (0.6%) and product fit (2.5%).

What's the most common mistake when Amazon sellers pivot to DTC?

Running a DTC site like an Amazon PPC channel. Amazon muscle memory — search term, bid, conversion — is a tight PPC loop that's worked for a decade. DTC needs different infrastructure: owned audience, SEO, repeat purchase mechanics, brand. In our dataset, 14 Amazon-to-DTC failures hit either single-traffic-channel or multi-factor 100% of the time. They carry the deepest PPC reflex: when traffic drops, the instinct is "spend more on ads."

Can AI agent data be trusted? How were the 300 cases validated?

171 raw records from 3 parallel agents → 6 cross-source duplicates removed → 6 landmark cases set aside for separate analysis → 159 entered validation (all passed: each requires a name, a confirmed shutdown date, an accessible source URL, and quantified financials where available) → human review removed 5 (4 confirmed alive via second source, including Bravo Sierra; 1 anonymous-only). Final dataset: 154 in the bankruptcy CSV + 13 landmark cases broken out = 167 named cases total. Every data point traces back to its primary source. Read more on why audit trails are non-negotiable when an AI agent makes consequential decisions.

If most DTC brands are failing, should sellers retreat to marketplaces?

The data has a counter-example. Bravo Sierra deliberately killed its Facebook ad spend after iOS 14, pivoted to omnichannel, raised a $17M Series B, and landed in Target and Walmart. The pattern isn't "DTC is dead" — it's "single-channel paid traffic is dead." Brands that build the math (LTV, repeat purchase, owned channels) keep working. The failure mode is treating the DTC site purely as an ad-buying destination.

Do landmark cases like Allbirds and RAVPower apply to small DTC operators?

Yes. Landmark cases are valuable not because of their scale, but because they amplify the same death path to the point that everyone can see it: Allbirds spent 35-43% of revenue on marketing, Outdoor Voices' LTV was 4.5x lower than Lululemon's, RAVPower's DTC pivot only recovered 23% of its Amazon revenue base. The underlying logic — CAC climbs faster than LTV can support it, so the unit economics collapse — applies identically to a $10K/month store and a $4.1B IPO. Small operators just die faster and don't get press coverage.

How long until I can know whether my DTC site is on this 95.5% path?

The four warning signals you can self-check this week: (1) paid traffic as a share of total sessions — if it's above 60% and rising, you're trending single-channel; (2) returning-customer revenue as a share of total — if below 25%, repeat is undersized for most categories; (3) CAC trajectory over the last 6 months — if it's up more than 30% and conversion isn't tracking up with it, the unit economics are eroding; (4) organic search traffic share — if it hasn't grown in 12 months, the compounding asset isn't being built. Three or more flags means you're in the 95.5% pattern.

Next Step

One opinion, take what's useful. The "thin traffic mix + missing repeat purchase" death path we sized in this analysis is also baked into Omni-Growth Agent's diagnostic logic — the AI agent runs the same checks across "Online Performance" and "Channel Opportunity Scan" modules and tells you, directly, whether your DTC site is currently walking this path.

If you're running overseas marketing today, you can run a free AI agent audit on your own accounts.